SMM, January 17: SMM has learned that since the concentrated and large-scale signing of orders for polysilicon in mid-December, market sentiment in the upstream polysilicon and PV sectors has continued to improve. Against the backdrop of some improvement in inventory, coupled with factors such as corporate self-discipline, polysilicon producers have raised their quotations. As of now, the highest quotation for N-type polysilicon has reached 45 yuan/kg, with recent market transactions also increasing to 42 yuan/kg compared to the previous round.

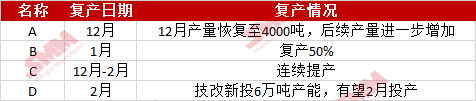

Stimulated by this situation, polysilicon producers have gradually started production expansion actions since December, with some long-idled bases even resuming production. According to SMM, starting from early December, excluding the expected ramp-up of new capacity, at least three polysilicon producers have initiated production expansion or reopening actions at some of their bases. Among them, a base in Xinjiang resumed mass production of polysilicon in December after about three months of shutdown, with a production of approximately 4,000 mt in December and over 5,000 mt in January. Additionally, a base in Inner Mongolia with a capacity of over 200,000 mt resumed operations to 50% in January after 5-6 months of shutdown. Meanwhile, a company in Ningxia also increased production in December and January, with expectations of full production in the future...

A newly added 60,000 mt technological transformation project has recently entered the equipment commissioning phase and is expected to bring new increments by month-end or February.

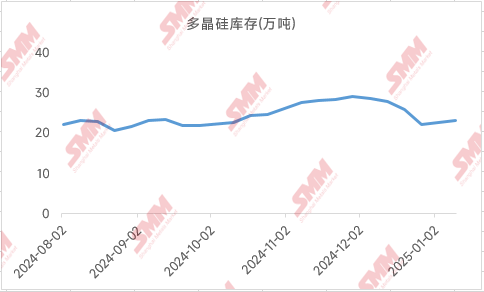

Some polysilicon producers are "eager to move," but can production truly recover? SMM believes that caution is still warranted for the current market situation. Firstly, the polysilicon industry still faces significant inventory pressure. Although producers experienced concentrated procurement earlier, there is still over 200,000 mt of inventory, and while crystal pulling plants have purchased large amounts of polysilicon, this raw material has not been promptly consumed but is instead being stockpiled as inventory for Chinese New Year or buying the dip. SMM data shows that raw material inventory at crystal pulling plants currently exceeds 200,000 mt, with some plants holding tens of thousands of mt in inventory. As the recent "final concentrated procurement" concludes, polysilicon faces significant order pressure, and the risk of inventory buildup for polysilicon producers is high. Subsequent inventory may return to over 300,000 mt.

Moreover, it can be observed that top-tier polysilicon enterprises do not appear to have taken significant production expansion actions, primarily maintaining stability. For February production, SMM statistics show a slight increase in the overall operating rate, but due to the impact of fewer days, actual production may slightly decline.

In summary, after this round of price increases and downstream procurement completion, there is still some resistance for polysilicon and even silicon wafers in the future. SMM believes that both transactions and prices are unlikely to see significant improvement before or after the Chinese New Year. For the March market, it will still depend on whether downstream demand can exceed previous expectations. SMM will continue to monitor developments.

》View the SMM PV Industry Chain Database

![[SMM Analysis] Philippines Accelerates Grid Connection for 1.28 GW of Solar](https://imgqn.smm.cn/usercenter/HfeeS20251217171739.jpg)

![[SMM PV News] EU Approves €500M Cleantech Scheme for Luxembourg](https://imgqn.smm.cn/usercenter/Jzkij20251217171737.jpg)

![[SMM PV News] Premier Energies Starts Trial Production at 5.6 GW Module Plant](https://imgqn.smm.cn/usercenter/Pjwqt20251217171738.jpg)